VPP Week-In-Review — Week of June 2, 2026

Your weekly brief on virtual power plants in the US & Canada.

Three Takeaways

Hyperscalers now have a contract structure for directly funding demand-side capacity: Voltus’s Google deal is the first proof point in PJM.

Billions spent on smart meters won’t unlock gigawatts of stranded residential and small commercial VPP capacity as long as PJM utilities block aggregators from accessing the data.

The biggest lever for VPP growth in a representative SPP utility isn’t technology. It’s friction reduction: a Brattle/Uplight report found enrollment and marketing improvements drive 59% of all incremental capacity potential.

News Roundup

Partnerships · 🟢

Voltus and Google to Deliver Grid Capacity Through Bring Your Own Capacity Agreement 📅 Published: June 2, 2026

Google has signed a three-year BYOC deal with Voltus to aggregate up to 100 MW of PJM-accredited DERs annually — the first time a hyperscaler has directly funded a VPP. Voltus absorbs the accreditation risk and delivers capacity via a contract structured like a standard PPA, which Google said was the commercial prerequisite no other aggregator could meet. The VPP goes live in 2027 and is designed as a replicable blueprint for other large-load customers facing the same capacity gap.

Utility Programs · 🟢

Massachusetts ‘vehicle-to-everything’ demonstration hints at EV batteries’ grid potential 📅 Published: June 2, 2026

MassCEC has begun deploying free bidirectional chargers to 4 municipal entities, 5 school districts, and 45+ residents under a two-year V2X demonstration — eligible vehicles include the F-150 Lightning, Kia EV9, and five e-bus models. Enrolled light-duty EVs can earn roughly $3,000 per summer via the ConnectedSolutions VPP; electric school buses can clear $12,000 annually. The school bus use case is already described as making “economic sense,” which makes fleet electrification and grid services planning decisions increasingly inseparable.

Research & Reports · 🟢

Customer experience, better modeling can boost demand-side portfolio: report 📅 Published: June 3, 2026

A new Brattle Group report commissioned by Uplight finds that stacking demand response, energy efficiency, and time-of-use rates can unlock 89 MW of additional demand-side capacity by 2030 for a representative SPP utility — moving from 3% to 5% of total system load. Enrollment-focused strategies alone (one-click enrollment, personalized outreach) account for 53 of those 89 MW. Brattle says the framework is directly portable to other RTOs, including regions with high data center load growth.

Regulatory & FERC · 🔴

Utilities aren’t sharing smart meter data in PJM. That’s a problem. 📅 Published: June 4, 2026

A Voltus and Mission:data Coalition complaint to FERC (filed October 2025) alleges utilities across PJM — including Exelon’s ComEd, PSE&G, and Duquesne Light — are blocking aggregators from accessing smart meter data needed to enroll residential and small commercial customers in demand response programs. The practical effect: Voltus had 20,000 customers enrolled at ComEd but could get only 4% through the utility’s data system, losing ~23 MW of capacity. Emily Orvis, Voltus VP of energy markets, says “gigawatts of capacity are stranded” across PJM.

Policy & Legislation · 🟢

As Energy Demand Rises, More States Turn to Virtual Power Plants 📅 Published: June 4, 2026

Inside Climate News rounds up this year’s most significant state VPP actions: Massachusetts Governor Healey’s March 13 executive order targets 3.5 GW of demand management (including VPPs) by 2035 — nearly 13% of the entire New England grid’s peak demand. Minnesota’s PUC approved Xcel’s CapacityConnect program on May 13, a first-of-its-kind utility-owned distributed battery procurement deploying 200 MW of 1–3 MW neighborhood-scale batteries. NC State’s Autumn Proudlove, who tracks VPP legislation nationally, calls 2026’s pace a “steady uptick.”

Regulatory & FERC · 🟢

Illinois Clean and Reliable Grid Affordability Act VPP tariff deadlines 📅 Effective: June 1, 2026

Illinois’s CRGA went into effect June 1, requiring ComEd and Ameren to file initial VPP tariffs by June 1 for ICC approval by June 30. The short-term program — scheduled to launch no later than June 30 — compensates participating storage customers at a floor of $10/kW of average dispatch. The long-term program (effective December 31, 2028) expands eligibility to smart thermostats, EV batteries, and other behind-the-meter devices. Note: ComEd had previously withdrawn a proposed VPP tariff in November 2025; the CRGA removes utility discretion on whether to file.

Product Announcements · 🟡

Eve — multi-DER orchestration platform by ev.energy 📅 Published: June 4, 2026

ev.energy has launched “Eve,” a four-module platform covering the full utility VPP lifecycle: business case modeling (Eve Insight), customer enrollment (Eve Programs), real-time multi-DER dispatch (Eve Sync), and settlement-grade M&V with regulatory reporting (Eve Ops). The platform claims 55+ utility programs in North America and Europe, including Con Edison, Avangrid, and Ameren, with ~95% US EV household reachability via its OEM/EVSE integrations. The “Plan and Defend” positioning — building the business case and the rate case filing on a single stack — addresses the two phases most utility DERMS platforms skip entirely.

📊 By the Numbers

100 MW — Annual DER capacity Voltus will aggregate for Google’s PJM VPP under the three-year BYOC deal.

$12,000 — annual VPP revenue potential for electric school buses enrolled in Massachusetts’ ConnectedSolutions program.

3.5 GW — Massachusetts’ demand management target (including VPPs) by 2035, per Governor Healey’s March 13 executive order.

$100B — estimated consumer savings over the next decade from better grid utilization through solutions like VPPs, per a Brattle Group analysis cited in the Voltus/Google press release.

$6B / 12M meters — what PJM utilities have spent installing smart meters that aggregators say they can’t access to enroll customers in demand response programs.

🗓️ On the Radar

June 30, 2026 — Illinois Commerce Commission deadline to approve initial VPP tariffs filed by ComEd and Ameren under the CRGA. First mandatory utility VPP program in the Midwest.

End of June 2026 — FERC intends to act on the large-load interconnection rulemaking (RM26-4) this month. The rule could define how AI data centers connect to the grid — directly shaping the capacity gap that the Voltus/Google BYOC model is designed to fill.

💬 My Take

In Voltus’s and Google’s BYOC announcement for 100 MW of annual capacity, they said they aim to establish a “repeatable path for other large energy users to follow.” How big could BYOC (sometimes called BYODC) be as a lever for VPP market growth? In context, Woodmac estimates that from 2024 to 2025 VPPs added 4.5 GW of incremental capacity. Assuming similar growth in 2026, this deal alone would be 2% of VPP growth in 2026. For this to be a meaningful growth lever, other organizations need to be able to offer similar kinds of contracts to hyperscalers so that offers can be standardized, driving down contracting costs and making it as simple as a solar PPA. My question is, aside from Voltus, who else in the VPP market can provide this type of contract offer for hyperscalers to create competition in the next year?

In a January 2026 Open Circuit Podcast Caroline Golin, Google’s former Global Head of Energy Market Development & Innovation, explained that when Google was looking for a VPP BYOC offering, only Voltus could provide a contract that Google would consider because they took on two key risks:

The aggregator needs to take on capacity accreditation risk. This means if a resource doesn’t qualify for capacity credit in the market, that’s Voltus’s problem, not the data center opperator’s. To evaluate this risk - what entities have the market expertise to take this on?

The aggregator takes on being able to do customer acquisition. This execution risk was critical for Google to consider this kind of offering. To evaluate this risk, who has the scale to add a similar size of 100 MWs annually?

In addition to which entities can take on these two risks, I think about where geographic demand is strongest to deploy this contracting structure.

Spoiler: I think this kind offer is going to be largely concentrated in PJM and there are likely 5 companies that have the capabilities to make this offer to Google or other hyperscalers in the next year.

Geography & accreditation risk:

My first gate for thinking about this question is where would this be most valuable in the next 1-3 years. Looking at Datacenter.fyi data center growth is most dramatic in Texas, Virginia, Ohio and Indiana. Most of these are either partially or completely in PJM. PJM’s capacity prices have increased dramatically with this increase in demand.

PJM also is likely for additional BYOC-contracts because of the market mechanism for a VPP provider to take on capacity accreditation risk. In a Sightline write-up of a presentation by Dana Guernsey, CEO of Voltus, one key enabler for this type of offering is market capacity accreditation like what exists in PJM. The accreditation is enabled by being able to assess locational constraints where the VPP would need to be located to offset capacity from a data center.

While Texas has clear demand, there are market barriers that make me skeptical. Texas has already implemented Senate Bill 6 that results in flexibility capacity coming online outside of a capacity market. Texas’s energy-only market also creates a barrier for VPP capacity accreditation. Between both of these, I am skeptical of a BYOC-style contract in Texas in the near term.

While less dramatic than PJM or Texas, parts of MISO and CAISO are also experiencing significant data center growth. They also have capacity accreditation for demand response that could enable experts in those markets to potentially take on similar risks. Each has challenges: CAISO’s bilateral contracting creates significant incremental complexity with a third party data center operator. State-level bans for third party DR in MISO’s territory block large parts of the territory from being commercially viable. I am watching these markets as a second tier for BYOC offerings. To construct a list of top organizations, I’m going to limit the list geographically to PJM.

Customer acquisition & execution risk:

Caroline’s point about customer acquisition raises a second gating item - what companies can add 100 MWs of capacity in PJM annually? There are 56 registered Curtailment Service Providers in PJM. Many of these are utilities and energy retailers that offer some DR. Retailers definitely have the customer relationships to build out this kind of offering and the balance sheet to take on capacity accreditation.

I’d argue retailers, however, would not be able to get comfortable with owning capacity accreditation risk in the time frame needed to sign a contract in the next two years without a partnership or acquisition to enable the type of DR capabilities Voltus has developed. There are three companies I’m watching from traditional retailers.

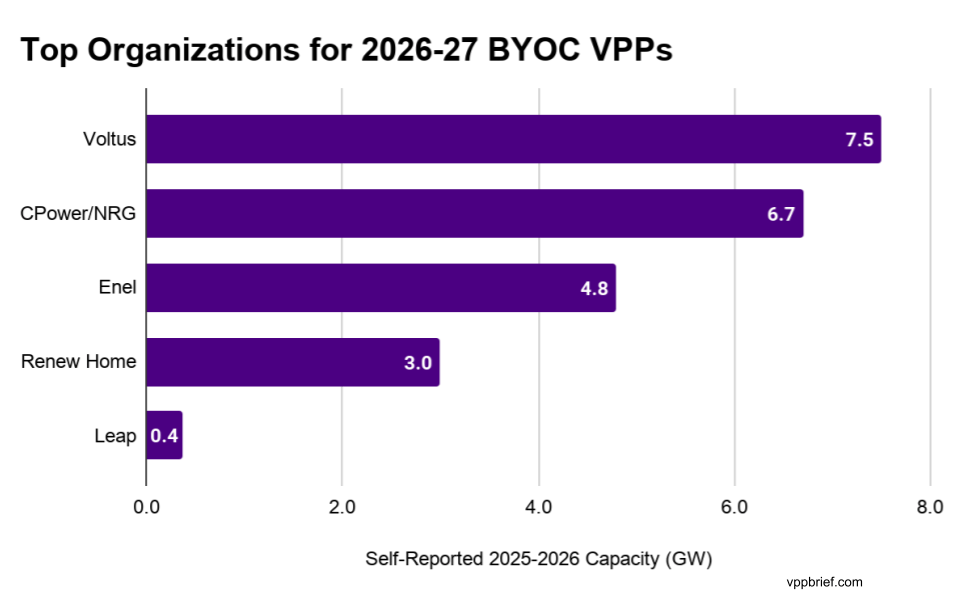

NRG acquired CPower and partnered with Renew Home in Texas to stand up a 1 GW VPP. They mentioned wanting to spin up a similar VPP in PJM. I think the combined CPower/NRG could put forward a compelling offering.

Constellation partners with GridBeyond in PJM, and they are targeting 1 GW of VPP capacity within 2 years. While they split out Nuclear and non-Nuclear capacity in their 8-k filings, they have no specific line item for total DR capacity. This indicates to me that their DR capacity is not meaningful enough today to put into regulatory filings. Given their lack of transparency on their current portfolio, I’d exclude them from the current list.

Shell’s MP2 has 575 MWs of dispatchable C&I load between PJM and ERCOT. Shell acquired Next Kraftwerke in 2021 and operates 15.5 GWs in Europe. However, Shell Energy and Next Kraftwerke haven’t announced any collaboration and Next Kraftwerke hasn’t highlighted any opportunities in North America. I would exclude MP2 because I think they lack the technical capabilities to be comfortable with taking on capacity accreditation risk.

The companies on this list that are aggregators with capacity can take on accreditation risk and have the scale to add this volume of capacity: Voltus, Enel, Renew Home (formerly OhmConnect) and Leap. Enel has retail relationships, is experienced enabling VPPs across the US at scale and has capabilities in house from their legacy EnerNOC acquisition to manage accreditation risk. I would expect Renew Home to explore a similar partnership for this kind of work in PJM given their prior partnership in TX and existing utility relationships through Rush Hour Rewards.

I should disclose I work at Leap, so weigh this section accordingly. That said: Leap’s partner ecosystem allows them to unlock capacity from other OEMs, aggregators and financiers. As a result they have doubled capacity year-over-year from 2024 to 2025. They also had a webinar in March, outlining the different monetization pathways for data centers they are pursuing.

Looking through press releases, this is a view on the size of each of these organizations’ existing capacity:

For BYOC to unlock meaningful VPP capacity, we need a competitive market for this offering. I’m optimistic that by the end of 2027 there will be at least 2 addional public BYOC contracts with entities on this list. If that happens, BYOC could start to drive VPP growth upward. If it doesn’t, I’m skeptical BYOC contracts will be meaningful to data center build out or the VPP market.

What Did I Miss — or Get Wrong?

Spot a story that should have been in this week’s issue? Disagree with the way I’m interpreting the facts? Just comment in notes with a link to the story or your take.

Opinions are my own and not the views of my employer. Research and drafting for this issue was produced with the assistance of Claude AI. All editorial decisions are mine.

Great read.